2nd Gen Intel Xeon Scalable Refresh Market Impact

Due to the size and scope of the refresh SKU list, Intel is clearly changing the competitive landscape of its refresh v. pre-refresh parts. The other obvious comparison is to the AMD EPYC 7002 series. At the same time, we believe this refresh can make inroads far beyond the two obvious competitors. It will impact the Xeon W-3200 and Xeon W-2200 series as well as the Xeon E-2200 series which is performance competitive with the Xeon Silver line. Finally, for every future Arm competitor, their point of comparison will need to change.

2nd Gen Intel Xeon Scalable Refresh v. Pre-Refresh Xeon Scalable

If you need 4-socket or 8-socket servers, the pre-refresh parts are for you. Consider these higher scale-up server parts much like the Xeon E7 series was previously. it is easiest to see these as Intel launched the Xeon E7 generation in 2019, now we get the analogous Xeon E5 generation at a lower cost in 2020.

In the two-socket markets, it will be extraordinarily difficult to purchase non-R SKUs outside of a few segments such as the Xeon Bronze 3204. The Xeon Silver performance bumps are great but perhaps the 100W v. 85W TDP will cause a segment of the market to still buy the 2019 generation parts.

For the mainstream dual-socket market, not impacted by high-memory parts, the new Gen 2R Intel Xeon Scalable (our term, not Intel’s) parts are clearly the way to go. Unless you need an L SKU for over 1TB per socket or you need 4/8 socket capabilities, the new Intel Xeon “Refresh” SKU stack is just the way to go. An example of the Xeon Gold 6230R to the previous generation Gold 6230 and Gold 6130 shows why. Intel is drastically increasing performance per dollar in this generation.

Again, given the feature differentiation, we think that Intel could have called this more than a “refresh” or additional SKUs and instead called it a new product line akin to the Xeon E5-2600 V1-V4 generations for mainstream servers versus the previous generation being closer to the Xeon E5-4600/ Xeon E7 lines.

For STH readers, the Xeon Gold R SKUs are a much better value than the older Xeon Gold and Platinum SKUs. It is awesome that Intel is doing this.

2nd Gen Intel Xeon Scalable Refresh v. AMD EPYC 7002

For AMD, the road just got tougher. Contrary to many beliefs out there, Intel does not have to meet or beat AMD’s performance per dollar in markets primarily focused on compute. Intel just needs to be close.

There are a few costs that one overlooks when looking at CPU prices only. For example, a ~$50 “Lewisburg” C62x PCH goes in every dual-socket Intel Xeon Scalable server. Intel also sells a ton of NICs and SSDs that go to big OEMs and end customers. Intel has FPGAs and other accelerators as well as Optane DCPMM.

Intel’s strategy is to create a giant silicon portfolio, then be able to bundle across. For AMD, it can have a better CPU, but if you have $2000 of CPUs in a server and $20,000 of SSD storage, Intel can make up CPU discounting on the bundle. It can also do this at a higher-level giving performance incentives across its portfolios to OEMs and channel partners.

Intel still does not have a great answer for the 64-core AMD EPYC parts since on a per-node basis Intel needs to get to 4-sockets to hit the same levels of performance. Still, for the mainstream 8-32 core markets, Intel now has a “good enough” answer, and that is going to force AMD to respond.

While Intel has AVX-512 and VNNI, it also expanded Optane DCPMM support down to a Silver-level SKU. That will further put pressure on AMD as Intel has a very good feature that is now more accessible even if it is simply as low latency and fast persistent storage.

AMD’s strengths are in PCIe Gen4 and having more memory bandwidth and capacity for mainstream SKUs. It also has an architecture that utilizes (relatively) a ton of cache which can make up for a lot of the clock speed delta Intel is pushing in this generation. AMD is the better value looking at CPUs, but one needs to really look at post-discounting system-level costs to see the benefit.

2nd Gen Intel Xeon Scalable Refresh v. Intel Xeon W-3200

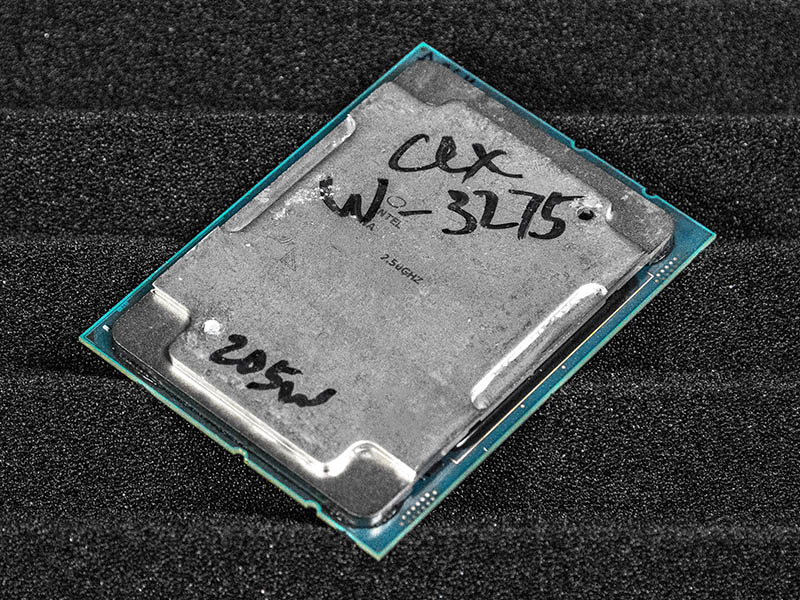

The Intel Xeon W-3200 series is now in a very strange predicament. Here is why. With the new price changes the SKUs in this series are now going to see a lot of pricing pressure. For example, the Intel Xeon W-3275 can have 64 PCIe lanes if the motherboard supports it which is great for a 28-core part that can hit 4.5GHz. Still, one can save around $500 and get the Xeon Gold 6258R and get a lower top turbo chip with other benefits. The Gold 6258R can be used in dual-socket servers which means more scalable performance and lower costs from using fewer systems. It can also support Optane DCPMM. If you wanted a high-end 28 core CPU with Optane DC Persistent Memory, the Gold 6258R is now a considerably better choice than the Xeon W-3275.

There is a chance this market will not care, or simply wants the higher low-core count utilization turbo numbers of the Xeon W-3275. On the other hand, Intel once again has very viable dual Xeon workstation models and pricing with the R parts.

2nd Gen Intel Xeon Scalable Refresh v. Intel Xeon W-2295

That discussion of the R parts moves down to the Xeon W-2200 series. Our review of the Xeon W-2295 is going to be online in the next few weeks, but this new “refresh” launch puts pressure on these chips as well.

The Intel Xeon W-2265 is a $944 part, with 12 cores a 3.5Ghz base clock and a 4.6GHz turbo clock. How does that stack up compared to the 16 cores 2.9GHz to 3.9GHz Xeon Gold 6208U with 50% more memory channels and bandwidth and DCPMM support?

Likewise, we will explore how the Xeon W-2295 at 18 cores compares to the 20 and 24 core Xeon 5218R and Xeon 5220R that sacrifice clock speed for cores and platform features.

The question Intel needs to answer for the Xeon W-2200 series is why should one invest in this platform versus just using LGA3647 which will be more robust.

2nd Gen Intel Xeon Scalable Refresh v. Intel Xeon E-2200

This may seem strange, but there is a good reason for this one. The Xeon E-2200 series like the Intel Xeon E-2288G can now hit 8-cores for $539 and at very high clock speeds. Still, the platform is limited to ECC UDIMMs instead of RDIMMs, and one must buy a node for every 8 cores and 95W TDP of CPUs. Now, one can purchase a 26 core Intel Xeon 6230R for $1,894 with a 150W TDP or a 24-core Xeon Gold 5220R for $1,555. While one loses per-core performance, it is going to be immensely less expensive to consolidate to dual Xeon Gold systems and virtualize than using Xeon E-2200 series servers.

Even the Xeon Gold 4215R with its 8 cores and Xeon Silver 4214R with 12 cores in the sub $750 market are going to make sense for users who want lower core counts and TDP, but also want more memory and platform I/O. A Xeon Scalable single-socket server costs more than a Xeon E-2200 platform, but it also has a lot more I/O and consolidation benefits that can reduce the impact in some segments.

2nd Gen Intel Xeon Scalable Refresh v. Future Arm Competitors

For any Arm server vendor that is using the Platinum 8280 as a “we are 60% less than Intel” their marketing message much change. The new appropriate 28-core Intel comparison point is the Xeon Gold 6258R which is over 60% less than the Xeon Platinum 8280.

Putting this another way, if an Arm vendor was claiming 70% better price/ performance than an Intel Xeon Platinum 8280, they now have a sub-33% benefit. What is more, like AMD the Arm vendors are going to have to contend with Intel’s bundling girth plus some switching costs, even given how much as the Arm ecosystem has matured recently. Is 33% enough if AMD without as much switching cost gained 5% market share in a few years with a better figure?

To the Arm ecosystem, the “refresh” is going to ravage comparison talking points using the Gold 6258R. Intel has needed to get that Platinum 8280 differentiated and seen as an 8-socket part to prevent list price comparisons since the first generation Platinum 8180 launched.

On the flip side, Intel has a solid chance to sell more “refresh” Gold SKUs before many of the next-generation Arm competitors are even available in the market than those Arm competitors will sell in 2020 combined. As they launch, they now have new marketing messages even before Intel transitions to Ice Lake Xeons.

Final Words

This launch of “refresh” CPUs is really a launch of an interim line between the 2019 2nd Generation Intel Xeon Scalable line and the allegedly 2H 2020 Ice Lake Xeon line. Let us call it what it is. Intel is facing increased market competition in the CPU segment. It needed to respond. The way it responded was by effectively re-launching the Xeon E5-2600 with dual-socket capable only parts at a lower price than the previously launched quad and eight-socket capable parts like the Xeon E7 family had.

Of course, in the world of microprocessors and manufacturing, the fact that these are still “Cascade Lake” generation microarchitecture parts means that we will call them 2nd Generation Intel Xeon Scalable, but let us be clear: this is a new sub-series of processors. 1-10% more performance per dollar has been a refresh. Hitting over 50% more performance per dollar is more than we saw generationally for almost a decade. This is effectively a new line.

By implementing DCPMM support further down the stack, Intel is signaling something obvious, that it is focusing on bundling silicon products. The more SKUs that support DCPMM the more opportunities to bundle that technology along with other technologies. Intel does not need to be the lowest cost on CPUs if it can provide the best value at the server and rack levels.

With this “refresh” or “Intel Xeon Scalable Gen 2R” launch, it is now up to the rest of the industry to respond. Make no mistake, this is a fierce and formidable competitive move by Intel and other players now need to respond in turn.

{kind=link}

This is the best coverage out there and I’ve skimmed Anand’s and Tom’s pieces. I wish you benchmarked more SKUs for it though but you’ve at least got something.

I’m with Teddy1974 and I read some analyst reports this morning too. I can’t believe this is free analysis.

Very nice article. What killing me is “Our review of the Xeon W-2295 is going to be online in the next few weeks” note inside it. I’ve slowly set on W-2295 as my workstation update (from old E5) hence would like to see your article rather soon than later.

Also W-22xx versus new “R” line, I think it’s matter of workstation preference. If the target software is more single-threaded oriented, then one may favor W-line for its higher turbo freq, however if the software is more multi-threaded and user is 100% sure about it, then investment into R line may make sense.

To put it bluntly, where is Cooper Lake? Wasn’t that supposed to be the stop-gap between Cascade Lake and Ice Lake? I know it was to be AI focused with BF16 support but is Intel squarely targeting only that segment for it? It’d be a means of getting a new platform out the door as well as negating several security issues that exist in Cascade Lake hardware.

Kevin, Cooper is coming. I think it is slightly different in market positioning at this point. All I can say for now is stay tuned to STH.

Too bad Patrick never mentioned DCPMM capabilities of these new CPUs

/s

Bored SysAdmin – 12 times in the article DCPMMs were mentioned including specific discussions. I am not sure what that comment means?

/s = sarcasm

/s is totally lost on me :-)

Great review. Thanks.

“For AMD, the road just got tougher. Contrary to many beliefs out there, Intel does not have to meet or beat AMD’s performance per dollar in markets primarily focused on compute. Intel just needs to be close.”

Really with Zen-3 Epyc/Milan sampling what’s going to happen after that and AMD’s Epyc/Rome pricing can go down even further what with those Zen-2 CCDs so easy to produce at such high Die/Wafer yields. AMD’s running a much leaner operation and TSMC’s process node R&D costs is amortized across an entire industry and not just AMD only. AMD’s response can be readily apparent and AMD’s economy of scale on those 8 core CCDs is testament to that. Intel’s 60%+ gross margins are no longer and if AMD’s Opteron competition was any indicator then that metric is going down further as well with Epyc at a level of parity in performance and at a price that Intel has now been forced to counter.

Currently as well some of AMD big Epic wins are going hand in hand with Nvidia’s GPU accelerators or even AMD’s Own GPU offerings for GPU compute that’s a bit more than any CPU can provide and Intel has not yet fielded any competition that has Nvidia shacking in it boots. AMD is really got the low overhead advantage in any price war what with Intel still on those monster monolithic designs that make the Die/Wafer yield calculator produce some sobering results.

The road has always been uphill for AMD and what’s new is that that hill is larger but AMD is about to crest for a good while and the going is not that bad when those CCDs only have 8 cores and mad Die/wafer yields and are scalable up to 64 cores on an MCM and probably higher if need be. Zen-3 is sampling and Zen-4 and Zen-5 have their own teams leapfrogging forward on a regular cadence. AMD has no large chip fab upkeep expenses in which to worry about and that’s good for any extra pricing latitude on AMD’s side. And this obvious move from Intel can be countered as AMD can afford to go lower to a point that high overhead Intel will have to go underwater for a while to match.

It’s maybe a little late for Intel as too much notice of Epyc/Rome is already producing results that Intel will not be able to quickly counter easily as in the past. I’d look to Intel’s large war chest only for the short term as Intel has to use more of that on process node and foundry retooling but price wars in the server market are certainly a rare occurrence that have the bean counters absolutely giddy since Epyc/Rome really turned up the competition after Epyc/Naples got AMD’s foot back in the door.

Really needed to be done on the Intel side, the parts were just not competitive for a large portion of the market. Intel-only shops began to look elsewhere, in some cases with larger refreshes went all in on Rome given the increase in performance and very significant cost savings.

Core count wise, they just can’t compete against the 64c Rome monsters. For VMware shops looking forward they also don’t have a 32c sku for optimized license utilization on smaller deployments.

Vendor hardware appliances aren’t as common as they use to be but almost all are exclusively Intel, with the newer models available better cost reductions.

@LowOverheadLarry: The only problem with your “theory” is the reality that Intel is making more money EVERY year that they have been producing 14nm chips!! Amd is NOT making nowhere near any money with Epyc and the market for 64 core chips is ridiculously small while Intel is still making many BILLIONS every year from 4,6 & 8 core laptop chips!!!

Epyc has been available for over 3 years while Intel has been producing inferior 14nm chips and they barely have over 5% market share for x86 servers worldwide!!

Amd has to start producing revenue in large numbers if they really want to compete with Intel in the long run.

The day of reckoning is in 2021 when 10nm Ice Lake comes out in huge numbers, then we will truly see how competitive Amd is with Intel in the server space as Intel still dominates with 5 year old 14nm xeon /laptop chips that the market is still buying in massive quantities regardless of the superiority of the Zen 2,3,4 platform!

More competitive pricing. Nice refresh meaning we don’t have to replace existing motherboards to accommodate these new SKUs for those of us on earlier releases of scalable. I’m on gen1 6130 16core 2.1 base 3.7 boost… and and to me it means eventual drop in prices on used gen1 6130 for my other open socket. Or I can sell off my existing single gwn1 6130 and upgrade to two refreshed 2020 silver 5000 series 20 or 24 core for not much more $ and use my existing mono.

Cooper lake will mean socket newer socket/mono required and new chipsets, so again I say it’s a nice refresh for those of us who adopted to earlier gen scalable.

AMD still kills it though with better price performance and features if ordering all new systems.

@lemans24, it’s not about Intel being large and making more money as we all know that Intel has money. But Intel is a high operating cost/high margins necessary business that has to have the 55%-60+% gross margins on higher markups in order to remain revenue positive and not drain its cash reserves.

It’s about AMD’s Epyc/Rome and soon to be Epyc/Milan and that modular CCD/DIE economy of scale and AMD not having any multi-billion dollar Fab up-keep costs. TSMC’s 7nm/smaller node R&D costs are not solely AMD’s burden as TSMC spreads that Fab/R&D upkeep cost across an entire industry whereas Intel has its expensive fabs’ upkeep and equally expensive process node R&D costs to shoulder on its own and that can drain cash reserves like nothing else for Intel.

AMD is fabbless and its Epyc/Rome and Epyc/Milan CCD 8 core die wafer yields are always going to be better than what Intel has with its monster monolithic Die production. AMD is such a low operating overhead business with, now, an Industry leading server CPU product line that’s levels above AMD’s past Opteron predecessors on the Price/Performance metric that got AMD up to around 23% of the server market share in the past. So now with Epyc/Rome and soon to be released Epyc/Milan Intel will have to contend with that and AMD’s Zen-4 Epyc/Genoa on 5nm by 2021 and Intel has already had/is planning layoffs because Intel’s high margin mark-ups are taking a hit and so will those revenues needed to run Intel’s high overhead operations.

AMD can turn a profit at 43% gross margins while Intel would loose billions at that gross margin level. So now Intel is dropping it’s server CPU markups like a brick just to match AMD’s Epyc/Rome price/performance metrics and AMD has Epyc/Milan ready and sampling to potential customers so Epyc/Rome can have its price lowered by AMD and AMD will not go revenue negative like Intel will be having to go in an attempt to stop the bleeding market share. Each and every week AMD racks up new Epyc/Rome cloud customer orders and Intel is still not able to ramp up enough production at 10nm and even 14nm to stop AMD’s market share gains.

Once the Wall Street Quants fully suss out Intel’s longer term Gross Margin basis points decline/decline potential Intel will really have to rely on its other non processor business units to maintain and server CPUs was/is Intel’s high margin holy cow that’s having to be priced significantly lower. So with each percentage of Sevrer market share lost to AMD that’s millions of dollars less revenue for Intel and millions of dollars more for AMD on the quarter to quarter balance sheets. TSMC’s 7nm and AMD’s modular/scalable CCDs are totally the very definition of economy of scale and since AMD is fabless and TSMC provides fab services to an entire market of fabless chip makers they all share in TSMC’s fab upkeep/node R&D costs amortizations.

You are not going to be able to go against AMD’s/TSMC’s economy of scale and that’s just economics there once AMD’s Epyc/Rome benchmarks proved that Intel is not able to compete at its traditional price points and the layoffs will continue at Intel as those massive operating overheads have to be reduced or Intel’s cash reserves will evaporate rather quickly. Chip fabs are the most hungry of operations to keep fed and at 7nm and lower that’s billions more compared to 14nm/above just to hit the ground running.

Comments are closed.