NVIDIA this afternoon reported its earnings for both Q4 of their 2026 fiscal year, and for their complete 2026 fiscal year. And like most NVIDIA earnings announcements over the past few years, it is a doozy.

The flagship company for the current AI boom recorded $68 billion in GAAP revenue for Q4’FY26, a 73% year-over-year increase. And the company’s full-year results were equally impressive, booking $216b for all of FY2026, a 65% jump from the year before.

| NVIDIA Q4 FY2026 Financial Results (GAAP) | |||||

|

Q4’2026

|

Q3’2026

|

Q4’2025

|

Q/Q

|

Y/Y

|

|

| Revenue | $68.1B | $57.0B | $39.3B | +20% | +73% |

| Gross Margin | 75.0% | 73.4% | 73.0% | +1.6pts | +2.0pts |

| Operating Expenses | $6.8B | $5.8B | $4.7B | +16% | +45% |

| Operating Income | $44.3B | $36.0B | $24.0B | +23% | +84% |

| Net Income | $42.9B | $31.9B | $22.1B | +35% | +94% |

| EPS | $1.76 | $1.30 | $0.89 | +35% | +98% |

And in terms of total profitability, things are even rosier. Thanks to NVIDIA’s gross margins recovering to 75% – a level few chipmakers have ever reached – the company booked $43b in net income for Q4’FY26 alone, a 94% year-over-year increase in profitability. That quarter added to an already impressive haul by NVIDIA for the year, leading to NVIDIA closing out FY2026 with $120b in net income – a 65% improvement over the previous year.

| NVIDIA Full Year FY2026 Financial Results (GAAP) | ||||

|

FY2026

|

FY2025

|

FY2024

|

Y/Y

|

|

| Revenue | $215.9B | $130.4B | $60.9B | +65% |

| Gross Margin | 71.1% | 75.0% | 72.7% | -3.9pts |

| Operating Expenses | $23.1B | $16.4B | $11.3B | +41% |

| Operating Income | $130.4B | $81.5B | $33.0B | +60% |

| Net Income | $120.1B | $73.0B | $29.8B | +65% |

| EPS | $4.90 | $2.94 | $1.19 | +67% |

In short, Q4’FY26 has been yet another record-setting quarter for the company. It is now NVIDIA’s 12th consecutive quarter of revenue growth – three straight years – and NVIDIA is forecasting that will go into a 13th quarter and beyond in FY2027.

As well, this quarter has also seen NVIDIA handily shoot past their own projections for Q4. While the company was forecasting $65b +/- $1.3b for the quarter – an amount which would have still represented significant growth for the company – the final total of $68b has exceeded even the top-end of NVIDIA’s revenue outlook. As a result, NVIDIA is not just clearing record revenues, but it is continuing to grow at a faster pace that NVIDIA itself was expecting.

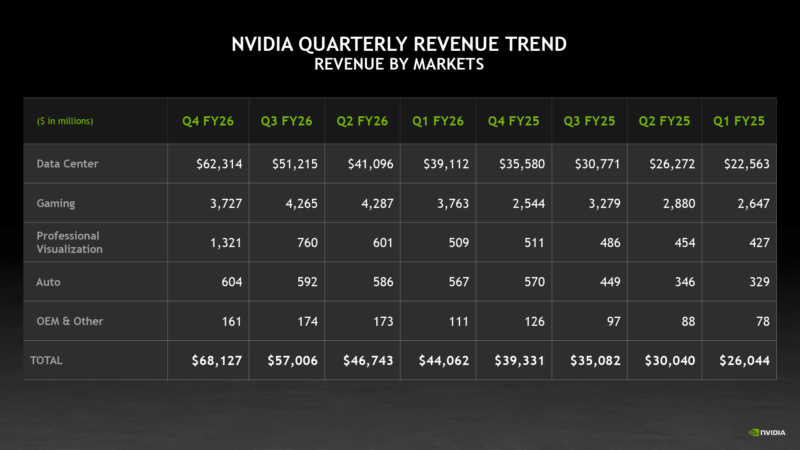

On the whole, then, NVIDIA’s top-line financials and many of their individual operating segments recorded record revenues. Of NVIDIA’s 5 operating divisions, the Data Center group once again led the charge here, and at this point makes up more than 90% of NVIDIA’s revenue – a problem that is anything but so long as it remains NVIDIA’s fastest growing division. Otherwise, the worst thing that you can say about NVIDIA’s financial situation right now – beyond whether they are growing fast enough to meet Wall Street expectations – is that in the cyclical consumer segments (e.g. gaming), Q4 is a weaker quarter than Q3 as retailers stock up for the holiday season roughly a quarter in advance.

As for NVIDIA’s shareholders, these record revenues have seen a good chunk of those profits returned to the shareholders in the form of stock buybacks – along with trivial cash dividends. According to NVIDIA, the company returned $41.1b to shareholders over their 2026 fiscal year. The remaining profits have been going several places, including investing in NVIDIA’s seemingly unstoppable growth and purchasing securities in other companies. But even then, NVIDIA’s cash and cash-equivalents war chest has grown by over $19b in the last year, and now sits at $62.5b.

Meanwhile, here is how things shape up for each of NVIDIA’s operating segments.

Data Center

For Q4’FY26, NVIDIA’s leading market platform extended its lead further, both in terms of percentage shares and in real dollars. With $62.3b in revenue for Q4 alone, Data Center revenues have grown by 75% year-over-year. At this point Data Center revenue is now 91.5% of all of NVIDIA’s revenue, not just returning Data Center revenue above the 90% mark, but resulting in the highest revenue share that the increasingly lopsided split has ever been.

At a high level, it would be fair to say that what has driven the bulk of this growth has been Blackwell, with everyone from hyperscalers to AI firms to rank and file enterprises seemingly unable to get enough of NVIDIA’s latest-generation server silicon. But outside of the official press releases and associated financial tables, NVIDIA’s CFO commentary for the quarter reveals an even more interesting trend: NVIDIA’s network revenue has been growing by an even wilder clip.

The company formerly known as Mellanox, NVIDIA’s networking division has been a large part of the technology stack that has enabled NVIDIA to scale up to NVL72 and other rack-scale (and beyond) designs. And as a result, while Data Center compute revenue is up by just 58% YoY, Data Center networking revenue is up by a staggering 263% YoY. NVIDIA proclaimed back in Q3’FY26 that they already had the world’s largest networking business, and that business has now grown by 34% in a single quarter.

As a result, compute’s share of revenue within the Data Center business has been on a decline. Whereas it was 91.5% of DC revenue in Q4’FY25, it is down to just 82.4% in Q4’FY26. In other words, despite all that growth in GPU (and Grace CPU) shipments, networking has moved from a sub-10% share to almost a fifth of all DC revenue.

NVIDIA has their fingers in many pies at this point, but do not be surprised to see this trend continue. Especially with NVIDIA rolling out Spectrum-X switches with co-packaged silicon photonics, the amount of cutting-edge networking gear that NVIDIA is slated to ship – even if only in service to their larger compute racks – is only going to increase.

Otherwise, 2026 will mark the continued ramp-up and sales growth of NVIDIA’s Blackwell Ultra GPU. Though by the end of the year attention will begin shifting to the Vera Rubin platform, which NVIDIA already soft-launched at the start of 2026 back at CES.

Finally, as NVIDIA closes out their 2026 fiscal year, it is interesting to note that amidst all of the success of the Blackwell architecture, the one product line NVIDIA has not been able to move are Hopper sales to China. After having been barred by the US Government from shipping even the export-friendly H20 to China at the start of the year, to being allowed to ship the far more powerful H200 by the end of it, NVIDIA is reporting very little in the way of sales in the back-half of the year – to the point that NVIDIA has published that they are “not assuming any Data Center compute revenue from China” in their Q1’FY27 revenue outlook. Elsewhere, H20 is mentioned in NVIDIA’s earnings as being “insignificant for both the third and fourth quarter of fiscal 2026,” and meanwhile Bloomberg is reporting that NVIDIA has been unable to sell a single H200 to China thus far.

Gaming

Unlike the ever-growing Data Center segment, NVIDIA’s Gaming segment has been staying a bit more down to earth. Though it remains NVIDIA’s second largest division by revenue by a significant amount.

For Q4’FY26, NVIDIA reported $3.7b in Gaming revenue, a 47% jump in revenue versus the year-ago quarter. Like virtually every other aspect of NVIDIA’s business, this was driven by the Blackwell architecture, with Q4’FY25 marking the calm before the storm of when the first GeForce RTX 5000 series video cards launched. As a result, it is only been for the past few quarters that NVIDIA has been shipping their Blackwell consumer parts in high volumes, with the ramp-up seemingly complete at this point.

Despite this, however, Gaming is one of just two divisions not to report an all-time revenue record for the quarter – gaming most recently peaked back at Q2’FY26. As the Gaming segment is highly cyclical due to holiday sales, this division normally sees a decline going from Q3 to Q4 as retailers finish stocking up for the holidays. And this is NVIDIA’s official explanation for the QoQ decline in revenue.

That said, however, we have also been witnessing the entire tech industry get squeezed by demand for AI hardware, which has left DRAM in particular in short supply. And while NVIDIA is insulated a bit from this due to contracts for GDDR7 DRAM, the entire PC building supply chain as a whole is not. As a result, NVIDIA is advising investors that the Gaming market is going to be seeing headwinds due to supply constraints in FY2026. Coupled with a drop in demand in some segments from higher overall PC prices, and it is likely that NVIDIA’s Gaming segment’s revenues will not be above $4b again for the foreseeable future.

Professional Visualization

Arguably the biggest surprise from NVIDIA’s Q4 earnings results has been their Professional Visualization (ProViz) business segment. Essentially the other half of NVIDIA’s graphics operations, ProViz was eclipsed by gaming long ago in terms of total revenue, and outside of COVID demand surges has been a somewhat stagnant business overall. None the less, it reportedly continues to be a high margin business for NVIDIA, making it more important than its smaller revenues would have indicated.

“Would have” being the operative phrase there, as ProViz has seen an explosion in revenue in the last 2 quarters. After setting an all-time record in Q3 at $760m in revenue, ProViz revenue has grown by 74% in a single quarter. For Q4, NVIDIA booked $1.32b in ProViz revenue, eclipsing all previous revenue records. As a result, it is not the Data Center segment, but rather ProViz that is NVIDIA’s fastest growing division – and that goes both for Q4’FY26 and for the entire year, at 159% and 70% YoY growth respectively.

NVIDIA is citing the “exceptional demand for Blackwell” as the key factor driving the growth of ProViz. With this segment encompassing NVIDIA’s RTX PRO video cards – Blackwell-based video cards that have far more VRAM than NVIDIA’s consumer cards – the RTX PRO lineup has been in high demand by system builders looking to run local inference for AI models. This is especially the case as 3GB GDDR7 chips have become available and give the latest cards a significant capacity advantage over earlier cards.

But the ProViz segment is also where NVIDIA records their DGX Spark system sales, with those systems becoming available a couple of quarters ago with production continuing to ramp-up. Unfortunately, NVIDIA does not provide a further breakdown of ProViz revenues, and while RTX PRO hardware is undoubtedly the bulk of revenue, it would be interesting to see how much the DGX Spark is contributing to that after a couple of quarters.

At any rate, while NVIDIA is not releasing any official guidance for the ProViz market, it will be interesting to see where revenues go in FY2027. Was Q4 a one-off fluke, or is ProViz now a regular one billion dollar per quarter business for NVIDIA?

Automotive and Robotics

The final NVIDIA business segment to record a revenue record for Q4 was NVIDIA’s Automotive and Robotics business, which at $604m for the quarter eked out just enough growth to pass Q3’s revenue record.

At this point, A&R may be the most consistent of NVIDIA’s businesses. $604m is only 6% revenue growth on a YoY basis – though the full year picture is rosier, with NVIDIA recording 39% more revenue for FY2026 than FY2025. FY2026 saw the release of NVIDA’s long-awaited Thor SoC, which in turn has spawned a new generation of Jetson, DRIVE, and other platform products. On the other hand, A&R is about the most conservative market segment – due in large part to safety and product continuity needs – which means it is slow to move one way or another.

For the moment, NVIDIA reports that they are continuing to see adoption of their self-driving platforms.

OEM & Other

Rounding out NVIDIA’s reporting segments, we have the OEM & Other category. This catch-all unit has been used to account for things such as sales of GeForce MX GPUs (i.e. ultra low-end dGPUs for laptops) as well as NVIDIA’s revenue from Nintendo Switch sales.

For the quarter, NVIDIA booked $161m in revenue, which was up 28% YoY. Similarly, the segment booked $619m for the entire fiscal year, which was up 59% versus FY2025. Unfortunately, NVIDIA is not providing any background information for this segment on this year’s reports, so there are no customers or product developments that the revenue growth can be concretely attributed to.

Outlook, Q1 FY2027

Finally, NVIDIA’s outlook for the first quarter of their 2027 fiscal year and beyond is quite rosy. The company is calling for $78.0b, +/- $1.56b in revenue for the quarter. Which, if NVIDIA achieves it, would be yet another quarter of record revenues for the company, beating Q4’FY26 by around 14% and marking 77% revenue growth over the year-ago quarter. And with NVIDIA expecting that their gross margins hold flat, it should also deliver on record profits, as well.

As with the past couple of quarters, NVIDIA’s position is that they are selling their products as fast as they can make them. Which is to say that the company continues to be supply-constrained across most of its product segments. This is not a bad problem to have for what is still a rapidly growing company, though it means that they are missing out on some sales that have gone to their rivals instead.

At the speed that NVIDIA’s product lines refresh, Q1’FY26 should be largely similar to Q4 in terms of the hardware mix. Still, NVIDIA is preparing for the launch of Vera Rubin this year, and that ramp-up is going to start making itself felt in NVIDIA’s product offerings and resulting financial performance. Hopefully we should have a better idea of just how soon that may be after next month, when NVIDIA hosts their annual GTC tech conference. Besides offering a better outline of the Vera Rubin timeline, NVIDIA often manages to throw out a few surprises as well – so it will be interesting to see what this year’s show brings for the company.

{kind=link}